")

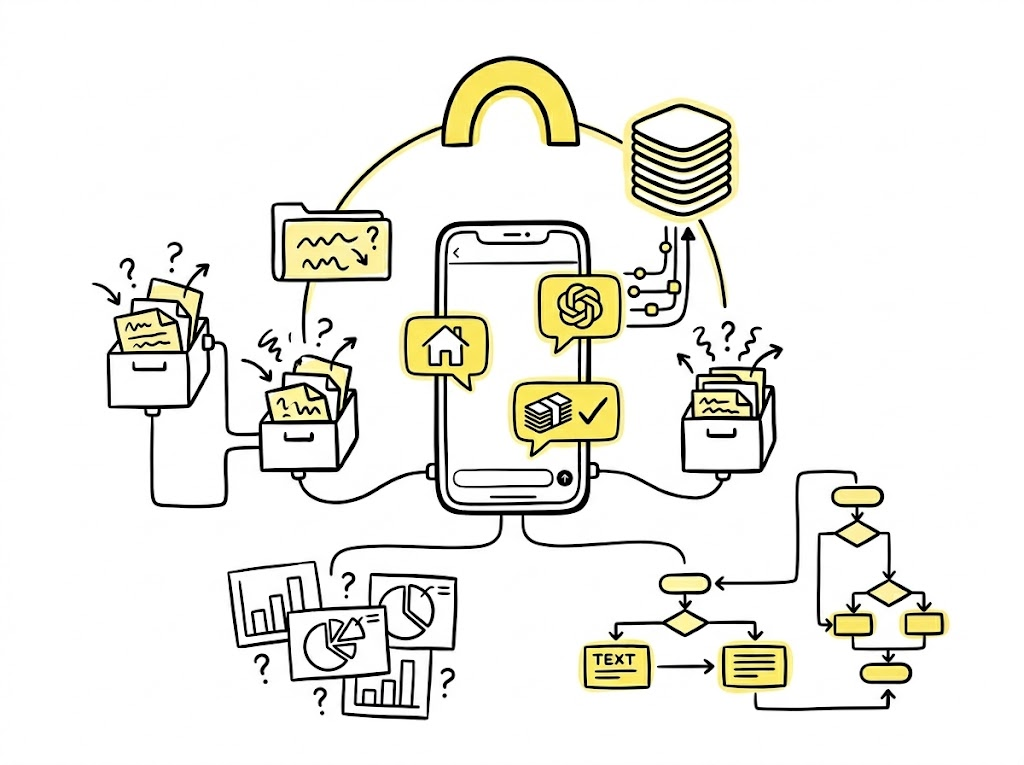

A few days ago, OpenAI announced a new personal finance experience inside ChatGPT powered by Plaid. U.S. Pro users can now connect their financial accounts and ask questions based on their actual financial situation. Not generic budgeting advice. Not “5 tips to save money.” Real-time answers grounded in someone’s own accounts, spending habits, debt, cash flow, and financial goals.

That changes the conversation quite a bit.

For years, AI in personal finance mostly lived in the “assistant” category. Budget reminders. Spending alerts. Predictive charts nobody looked at after week two. This feels closer to AI becoming the interface itself.

Instead of opening five banking apps and manually piecing together what is happening financially, users can simply ask: “Can I realistically afford a house next year?” or “What is the fastest way for me to pay off debt without killing my savings?” That sounds small on paper, but in reality it changes user expectations completely.

The Most Important Part Is Not The Chatbot

The real story here is infrastructure.

Financial data is messy. Extremely messy. Transaction descriptions are inconsistent, categories are often wrong, and most raw banking data is borderline unreadable unless heavily processed. One transaction says Starbucks. Another says SQ*TST12345. Another looks like someone smashed their keyboard.

Plaid is trying to position itself as the layer that translates all of that chaos into something AI can actually understand. And honestly, this is where the announcement becomes strategically interesting.

A lot of companies can build AI interfaces now. Far fewer companies have trusted access to financial data, institution connectivity, transaction intelligence, and consumer permission systems all working together. That combination is much harder to replicate than a chatbot UI.

Banking UX Suddenly Looks Old

Traditional banking apps already felt clunky before this. Now they risk feeling prehistoric.

Most banks still rely on dashboards designed around navigation. Tabs. Menus. Filters. Static charts pretending to be insights. But consumers are quickly getting used to conversational software that gives direct answers instead of forcing them to hunt for information.

Nobody wants to spend twenty minutes analyzing spending trends manually if they can ask one question and get a contextual explanation instantly. The last decade of fintech focused heavily on convenience. The next phase probably focuses on interpretation. Helping users understand what is actually happening with their money and what actions make sense next.

That is a much harder problem.

The Pressure On Fintech Just Increased

This also quietly raises the bar for every fintech product in the market. Once users experience financial tools that understand context deeply, generic experiences start feeling shallow very quickly.

Consumers will increasingly expect products to understand their full financial picture, personalize recommendations in real time, explain tradeoffs clearly, proactively surface useful actions, and adapt to changing financial behavior automatically.

And importantly, they will expect this everywhere. Inside neobanks. Inside lenders. Inside investment apps. Inside accounting platforms. Inside payroll tools.

The companies that win from this shift probably will not be the loudest AI brands. They will be the ones that make financial complexity feel simpler, calmer, and genuinely useful without crossing the line into creepy automation.

Key Takeaways

- AI in fintech is moving from generic guidance to context-aware financial intelligence

- Plaid is evolving from connectivity provider into AI infrastructure layer

- Conversational finance may replace traditional dashboard-heavy banking UX

- Consumer expectations around personalization are about to rise fast

- Fintechs now face pressure to make products smarter, not just prettier

If you’re building a fintech startup and want help refining positioning, messaging, or growth strategy, reach out.